Posted under: IPP

Ryan Ackers | SVP, Growth & Corporate Development, GBL

For the better part of a decade, Canadian business owners and incorporated professionals have been operating under a corporate tax framework that increasingly disadvantages passive investment income held inside their corporations.

The Tax on Split Income (TOSI) rules introduced in 2018, the passive income grind on the Small Business Deduction (SBD), and the steady integration of T4 and dividend tax rates have collectively narrowed the set of effective tax planning tools available to incorporated Canadians. And more recently, changes to the Capital Gains Inclusion Rate were pondered by the Ministry of Finance, before being abandoned (for now).

One of the most powerful remaining tools for the business owner is the Individual Pension Plan (IPP). For incorporated business owners and professionals aged 38 and over with consistent T4 income, an IPP can dramatically increase tax-deferred retirement savings, generate large corporate tax deductions, and reduce passive investment income inside the corporation, all while providing the predictability of a more flexible defined benefit pension.

Enjoy this updated version of our 2019 All Eyes on the IPP article. It has never been more relevant than it is today.

An Individual Pension Plan is a registered defined benefit (DB) pension plan. It is typically set up for business owners and incorporated professionals, where the sponsoring corporation funds future retirement benefits.

The Income Tax Act permits IPPs to use the most generous benefit formula available in Canada: the 2% Defined Benefit. An actuary calculates the exact contributions required each year to fund those promised benefits.

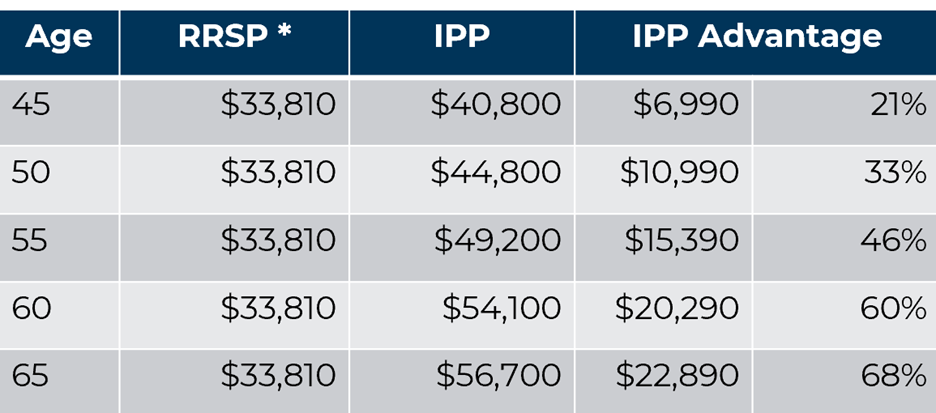

Unlike an RRSP, which has a fixed annual contribution limit ($33,810 in 2026), the contribution to an IPP is determined by the cost of funding the pension. Because that cost rises with age, salary, and years of service, IPP contributions substantially exceed RRSP limits.

The ideal IPP candidate typically meets the following profile:

Note: Pure dividend-only compensation will not generate contribution room for an IPP. The structure requires an employer-employee relationship and T4 income to form the basis of the pension calculation.

While RRSP contributions are fixed at a maximum of $33,810 (for 2026) regardless of age, an IPP contribution scales. From age 38, the IPP limit overtakes the RRSP limit. By age 65, the IPP contribution can exceed the RRSP limit by approximately 67%.

Note: IPP figures are illustrative for 2026 and assume the member is at or above maximum T4 earnings ($187,800 in 2025 income, the threshold to maximize 2026 RRSP room). Actual IPP contributions are determined by an actuarial valuation specific to each member. Contact GBL for a personalized analysis.

Every dollar contributed to an IPP is fully tax-deductible to the sponsoring corporation. The tax refund from these deductions typically exceeds the annual cost of the IPP. All contributions and fees are tax deductible:

The IPP provides several risk-mitigation features that are not available in an RRSP:

If for example, the business owner’s children work for the family business and earn T4 income from it, they can be added to the same IPP as their parents.

If the mother and father are drawing down from their IPP at the time of their passing, there is no taxable disposition upon the last parent’s death. Their assets stay in the IPP until a later date when the children decide to retire and draw down from the IPP.

This is an extremely powerful way to pass money down to the next generation tax effectively, but it requires the children to have a legitimate employer-employee relationship with the IPP’s sponsoring corporation.

Are IPPs flexible if my business has a bad year? As discussed in our 2019 All Eyes on the IPP article, yes. For “Connected Persons” (typically the business owner and family members employed with the business), contributions are not strictly enforced in most Canadian provinces, providing flexibility during leaner cashflow years.

Is an IPP Expensive? Can I deduct IPP administration fees? Unlike RRSP management fees, all investment management, actuarial, and administration fees associated with an IPP are 100% tax-deductible to the sponsoring corporation. This typically negates the cost of the IPP, making the fees cost-neutral in most cases.

Can I access IPP funds prior to retirement if I need them?

Generally, no. CRA mandates that the assets held within the IPP are there for retirement and you can have comfort knowing that those assets will be there when you need them in retirement. However, there are several options to unlocking IPP assets, including winding the IPP down into a LIRA (the amount that can be unlocked is determined provincially), and in the case of hardship, making an appeal to CRA to unlock assets.

How do I explore if an IPP is right for me?

Speak with your financial advisor and/or accountant to determine if the IPP is a fit. GBL completes complimentary IPP illustrations which will show what you can expect from contributions and retirement assets. You can assess the IPP illustrator to obtain an illustration here.

The Individual Pension Plan was a powerful tool when this article was first written in 2019, and the case for it has only strengthened with time. The corporate tax rules that drove business owners to look for new planning tools, the passive income grind, integrated T4 and dividend rates, and TOSI, have settled in as permanent fixtures of the corporate tax landscape. The IPP remains one of the most effective vehicles for incorporated Canadians to extract income from their corporations tax-efficiently while building a substantial, secure retirement.

For business owners and incorporated professionals aged 38 or older, earning $100,000 or more in T4 income, an IPP analysis should be a standard element of any corporate tax and retirement planning review.

Ryan Ackers is the SVP of Growth & Corporate Development at GBL, a national boutique actuarial consulting firm headquartered in Calgary, Alberta. He is the author of the original and updated All Eyes on the IPP articles.

Founded in 1995 and headquartered in Calgary with offices across Canada, GBL is a boutique Canadian actuarial consulting firm and a Canadian leader in compensation and benefit strategies for business owners, incorporated professionals, and corporate executives and employees.

GBL is Canada’s largest provider of Individual Pension Plans (IPPs) and Retirement Compensation Arrangements (RCAs). Furthermore, GBL provides retirement, health, and cross-border solutions including Defined Benefit and Defined Contribution pension plans, Supplemental Executive Retirement Plans (SERPs), Fair Market Valuations of Life Insurance (FMVs), health benefits, marriage breakdown calculations, commuted values, and expert witness services.

GBL positions itself as a boutique alternative to large multinational firms, delivering senior-led actuarial expertise with personalized service and competitive pricing. Visit www.gblinc.ca or call 403.249.1820 to discuss whether an IPP is right for you. www.gblinc.ca