Retirement Compensation Arrangement (Funded) vs Notional Accrual (Unfunded): This is a question that GBL frequently gets asked when helping companies design compensation packages. The answer depends on your company’s and employee’s individual circumstances.

For executive retirement planning, providing entitlements above the base defined contribution limits for high earning executives can be challenging. With maximum limit plans in Canada (2% Defined Benefit or 18% Defined Contribution), our limits for normal pensions max out at $187,833 of T4 income for 2025. To supplement these limits in a tax efficient manner, employers can establish a Supplemental Executive Retirement Plan (SERP) to provide enhanced retirement benefits above the registered maximums. In setting up a SERP, employers are often looking at 2 options: A Funded SERP through a Retirement Compensation Arrangement (RCA) and an Unfunded SERP.

An RCA is the vehicle required under the Income Tax Act to fund a SERP. A SERP is a papered promise to provide a certain amount of benefit to executives as a spillover to an existing defined benefit plan, group RSP or defined contribution plan. SERPs can exist in 2 forms: Funded and Notional (Unfunded). The funded plan uses an RCA as the vessel the benefit is funded into. Think of a SERP in terms of a program for an Executive Group that sets out the terms of the plan (funding, vesting, retirement).

For purposes of this discussion, we will compare RCAs to Unfunded SERPS.

An RCA is a retirement plan permitted by the Canada Revenue Agency (CRA), which can be used to set aside earnings for retirement on a tax deferred basis. Like an RRSP, income tax is not paid on income deposited into an RCA, and taxes are only payable on the withdrawals once they commence in retirement. Whilst the money remains in the RCA, it can be invested. Unlike with an RRSP, the contribution room generated in an RCA can be significantly larger and often reaches into the millions.

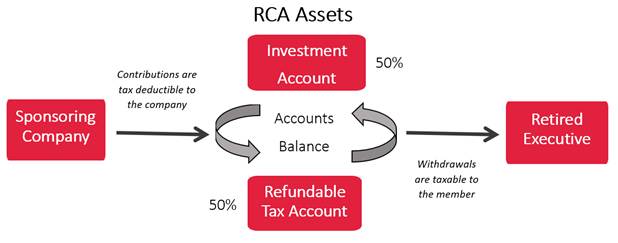

The RCA is set up by the employer as a retirement trust for the benefit of the employee to supplement future retirement income needs. Once the application for an RCA is filed with CRA, a Refundable Tax Account (RTA) is established for the RCA. The diagram below illustrates the structure of the RCA:

Contributions to the RCA are made on a payroll basis with the employer where at each pay period, 50% of the desired amount is contributed to an Investment Account (IA) held by the RCA Trust and 50% is remitted to a non-interest-bearing account with CRA called a Refundable Tax Account (RTA). Any realized investment returns are also subject to 50% refundable tax. CRA will hold 50% of these assets in the RTA. These funds are still assets of the RCA trust, but do not earn interest. Conversely, realized losses would see the RTA return 50% of the loss from the RTA back to the Investment Account. The key part to remember is that at the end of the tax year, both the IA and RTA must balance.

On retirement, as funds are withdrawn from the RCA, the IA is reimbursed from the RTA so the two accounts remain balanced. All funds paid from the RCA are subject to income tax rates in the year received. Whilst only 50% of the RCA assets are invested in the IA, the gain in after-tax income can often offset this perceived loss.

The advantages of the RCA are that it is a funded arrangement where contributions are made throughout the year so that budgeting is taken into consideration. For example, funding a $1 Million benefit over 15 years. The contributions are deductible to the sponsoring company in the year they are made.

If the preference is to fund the promise over smaller deposits over time, the RCA is an excellent vehicle. Also, as the RCA is a funded arrangement, the options for investments and portfolio options would be wider in scope. This would open the 50% invested to higher returns and lower investment fees which would be savings to the sponsoring company.

By funding an RCA, this provides additional benefit security for the member, as the funds are held outside the company in an RCA trust, ensuring that regardless of what happens to the company, the promised SERP benefit is secured through the RCA.

Through plan design, vesting can be incorporated so the member must meet a certain criterion to be eligible for the RCA benefit. If unvested, it is returned to the sponsoring company and therefore the company can still recover a funded RCA benefit if the vesting requirements are not met.

The downside of the RCA would be that only 50% of the contributions would be invested. As well any realized capital gains, interest and dividends would be subject to 50% refundable tax.

With that said, in most provinces in Canada, if the client is at, or close to the highest marginal tax bracket, they would pay close to, or more than 50% in tax without the RCA, so while the RTA is certainly a downside, the member will be better off with the RCA in many cases, especially if their income is expected to drop in retirement.

Other popular cases in which RCAs are used are Executive Severance, Sale of a Business, Expats, and Professional Athletes (particularly NHL Players).

The Unfunded SERP is promise to pay a benefit by retirement or termination. It is an earmark that sits on the sponsoring company’s balance sheet until it is paid out. An RCA could be used in retirement to fund the promise, or the promise would be paid out of general revenue over retirement.

In this scenario, the company would track a notional benefit, without physically securing the benefit with funding. There would be no immediate cash outlay, but also no deduction for any contributions. The notional account generally grows at a set interest rate, since unlike an RCA, there are no funds invested in an account. The rate would be agreed upon by the company and member at establishment of the SERP.

At retirement, the notional balance could be funded into an RCA, or paid out under the terms of the SERP directly from general revenue as payroll to the retired member. Over the lifetime of the SERP, the company would need to report the SERP obligation as a liability on the books since the benefit is not secured or funded.

With an unfunded SERP, there would be a promise to fund the specified benefit over the specified time period. There would be notional amounts contributed to the plan annually and notionally it would be the entire balance (100%), not 50%, that earns the set interest rate. This unfunded arrangement can be either secured by a letter of credit by the sponsoring company or unsecured where the promise is not backstopped by a letter of credit.

The sponsoring company does not need to fund the benefit immediately and can use the funds internally for working capital, corporate investments, or company growth.

The downside of the Unfunded SERP is that it would require full funding of the amount at or during retirement or termination. Depending on cashflows at time of funding, this could potentially be problematic. The company is not only responsible for the required funding amount but also required to guarantee any investment return on the SERP over the working years. If the set interest rate is greater than the company is receiving internally, this could create an additional obligation to the company.

The company must also report the SERP obligation as a liability on their tax reporting and financial statements.

If they do elect to secure the benefit with a letter of credit, additional fees apply with respect to the letter of credit.

For the member, if the unfunded SERP is not funded into an RCA at retirement but rather paid over a period out of general revenue, this provides much less flexibility on benefit withdrawals in comparison to an RCA as the member cannot elect when, and how much to withdraw as they see fit. The member must also be mindful of the potential that the company could experience severe financial hardship at the time in which the SERP is to be funded, which could lead to the loss of SERP assets.

There is no right or wrong answer. Each option makes sense in different circumstances. GBL will work with you to help determine the best option for you and/or your client. Contact us to learn more.

Founded in 1995, GBL is a leading provider of retirement, health, and cross-border solutions for business owners across Canada, and corporate pension administration. With offices in Calgary and Toronto, we have served 7,000+ clients, have 3,000+ Financial/Investment Advisors in our network, actively manage 2,000+ IPPs and RCAs, and have created 1,000+ HBPs and 3,000+ FMVs. We’re known for our industry leading client service and administration, as well as our top-notch actuarial group. Contact us today at info@gblinc.ca or 403.249.1820 and follow us to learn how we can help Build Your Future. www.gblinc.ca